Two sides of the coin - The Sri Lankan Rupee depreciates further

Pirakash Vivekananthan, Research Analyst, Founder & President of Tamil Economic Forum

This article examines the long-term behavior of the Swiss Franc (CHF) relative to the Sri Lankan Rupee (LKR). As the Tamil Economic Forum is based in Switzerland, the Swiss Franc is used as the base currency. Future publications will extend this analytical framework to additional currency pairs. The chart illustrates the CHF/LKR exchange rate, expressed as Sri Lankan Rupees per Swiss Franc.

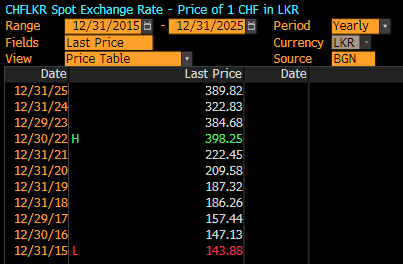

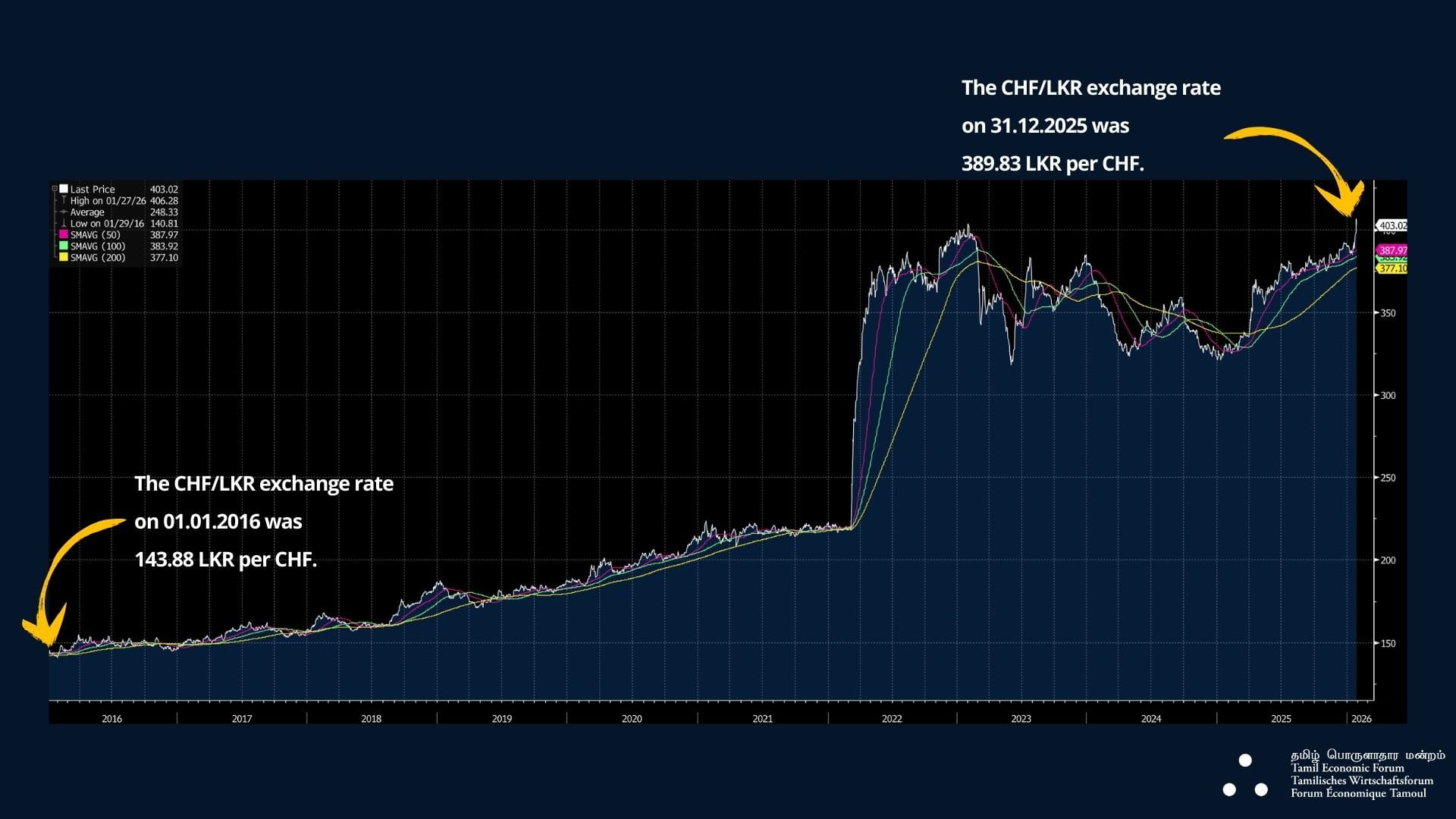

The chart shows the CHF/LKR exchange rate starting on 01.01.2016 at 143.88 LKR per CHF and reaching 389.83 LKR per CHF by the end of 2025. During the current week, the exchange rate crossed above 400 for the second time, after first reaching this level in early 2023, and currently stands at approximately 403 LKR per CHF. Over the period from 31.12.2015 to 28.01.2026, the Sri Lankan Rupee depreciated in value against the Swiss Franc by approximately 180% in cumulative terms, corresponding to an annualised depreciation of around 10.7% per annum.

For any currency pair, there are two sides to the coin, and this is equally true for the CHF against the LKR. From a consumer perspective, sustained appreciation of the Swiss Franc translates into higher purchasing power in Sri Lanka. For households planning travel in 2026 - whether for holidays or family visits - overall costs are likely to be lower compared to the previous year.

From an investment perspective, the implications are structurally different. Switzerland-based investors allocating capital to Sri Lanka over the past decade have faced an average annual adverse currency movement of approximately 10%, based on historical exchange-rate data. This currency effect represents a persistent headwind that must be incorporated into any long-term return expectations.

From the viewpoint of a Switzerland-based investor considering investments in Sri Lanka, the annual adverse movement of the CHF/LKR exchange rate can reasonably be estimated within a range of 8 - 12% per year. To achieve a net positive return in CHF terms, investment returns must therefore exceed at least 10% per annum in Sri Lankan Rupees.

In contrast, for consumers whose exposure is primarily through spending rather than capital allocation, this currency trend remains favorable and supports higher real purchasing power in both the near and long term.

TEF concludes that currency strategy is decisive. For investors, the CHF/LKR exchange rate constitutes a binding constraint on achievable returns. No matter how well a business performs, the falling Sri Lanka Rupee limits the actual profit a Swiss investor can take home. For consumers, by contrast, the exchange rate represents a persistent structural advantage, as the strength of the Swiss Franc consistently enhances local purchasing power.

Article written by Pirakash Vivekananthan